December 30, 2025 — By XGC Newsroom

The voluntary carbon market (VCM) has moved from its messy adolescence into a period of maturity and rapid scaling. During the first half of 2025 companies retired more credits than in any prior equivalent period, while more than USD 10 billion was publicly committed to new project financing. This influx of retirements and capital coincided with tighter integrity standards and greater policy alignment, producing a market that is larger, more disciplined and more consequential than ever before.

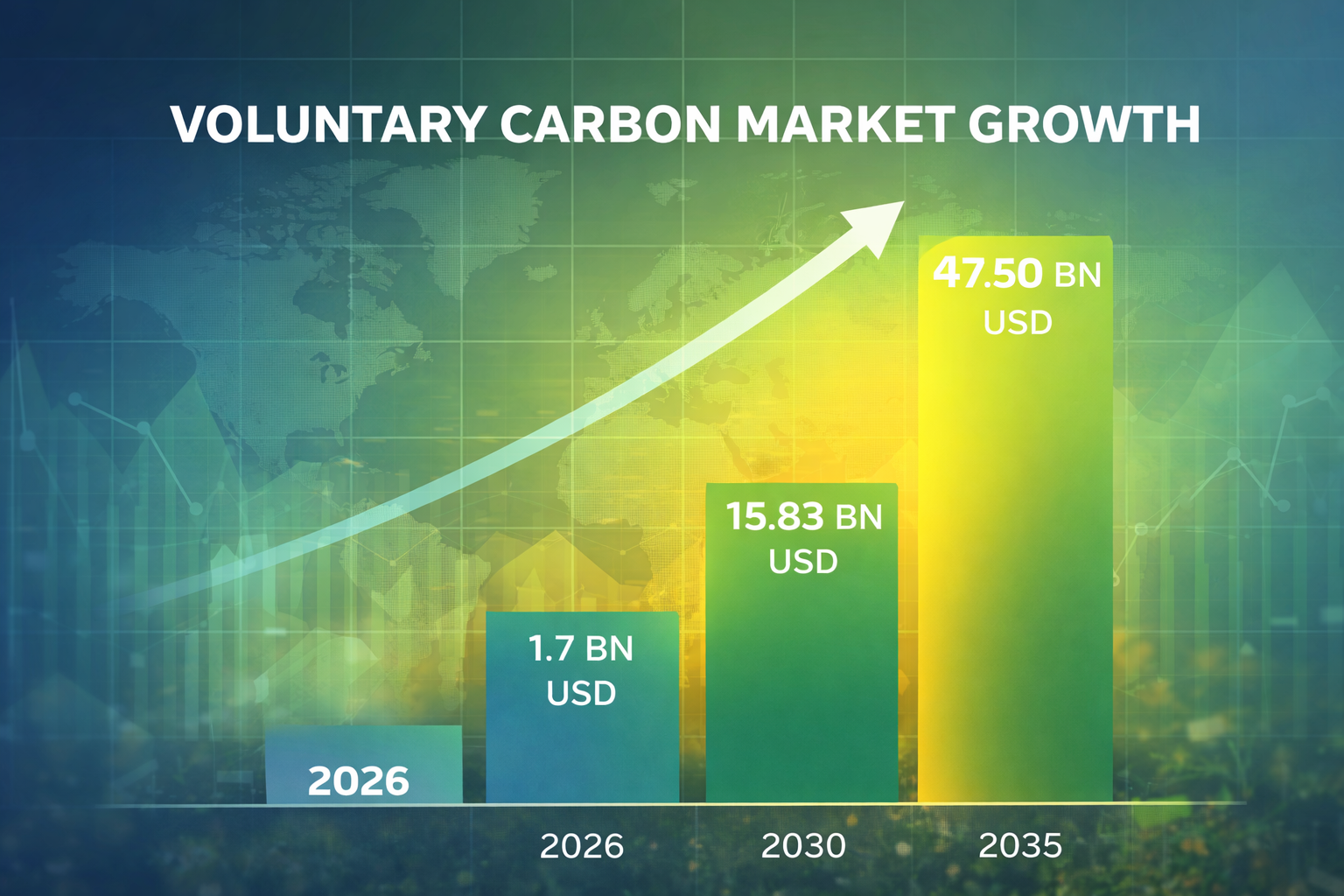

Market Size and Growth: A Spectrum of Forecasts

Analysts no longer question whether the VCM will grow; the debate now centres on how fast and how far. Roots Analysis values the market at about USD 1.7 billion in 2026 and expects it to climb to USD 47.5 billion by 2035. On the other end of the spectrum, Mordor Intelligence projects a base size of USD 15.83 billion in 2025 , rising to around USD 23.8 billion in 2026 and surging to USD 120.47 billion by 2030. Regreener and other boutiques fall in between, pegging 2026 around USD 3 billion but still growing at more than 20% CAGR. Disparities stem from differences in credit types and transaction definitions, yet the trajectory is unanimous: the VCM is shifting from a niche commodity into a core component of climate finance.

To visualise this trajectory we’ve created a simple conceptual bar chart (below). While not drawn to scale, it illustrates the steep growth expected between 2025, 2026, 2030 and 2035.

The conservatism of Roots Analysis reflects its focus on verified, premium credits. Their forecast emphasises high‑quality removals and removal‑heavy portfolios backed by more than 6,200 companies with science‑based targets. By contrast, Mordor Intelligence broadens the scope to include large volumes of avoidance and reduction credits, projecting a 50 % CAGR from 2025–2030. These divergent estimates highlight the importance of understanding market segments and underlying drivers.

Project Types, Transaction Modes and End Users

The VCM is not a monolith; its growth depends on the mix of projects, transaction types and buyers. According to Roots Analysis, renewable energy projects currently hold more than 30% share of the voluntary carbon credit market, reflecting their maturity and predictable output. Mixed transactions — combinations of removal and reduction credits packaged together — capture the largest transaction share. Industrial applications dominate demand, with the industrial sector responsible for the largest slice of credit usage. Private companies account for nearly 45% of current end‑user share, while governments, non‑profits and individuals comprise the rest.

Mordor Intelligence offers further granularity. In 2024, avoidance and reduction credits commanded about 69.4% market share , yet removal credits are expected to grow at a 55.9% CAGR through 2030. Renewable energy projects retained a 39.1% share , but waste‑management and methane‑avoidance initiatives are projected to grow at a brisk 52.6% CAGR . Corporate net‑zero commitments absorbed 60% of demand in 2024, while consumer goods and retail companies are forecast for a standout 54% CAGR to 2030. North America accounted for 37.5% of the market in 2024, with Asia‑Pacific projected to compound at 58.4% CAGR through 2030.

Why Companies and Individuals Participate: Advantages and Innovation

The voluntary market allows businesses, households and organisations to offset unavoidable emissions by investing in projects that reduce or remove greenhouse gases. The appeal lies in its flexibility: entities can support afforestation, blue carbon, clean cooking, clean water, reforestation, land protection and renewable energy initiatives. These projects not only mitigate climate impacts but also foster biodiversity, strengthen local communities and encourage innovation. In short, voluntary credits provide an accessible bridge for actors who cannot immediately eliminate their own emissions but wish to contribute to global decarbonisation.

Developers are responding with creativity. Root Analysis notes that voluntary projects span regenerative agriculture, blue‑carbon mangrove protection, high‑efficiency cookstoves and even wastewater methane capture. Mordor Intelligence emphasises that digital monitoring, reporting and verification (MRV) platforms integrated with blockchain can reduce issuance cycle times by up to 90%, dramatically cutting costs and improving transparency. Satellite imagery and IoT sensors continuously monitor forest biomass and soil carbon, providing near‑real‑time assurance to buyers. These technologies broaden supply diversity by enabling smaller projects to meet issuance thresholds and by connecting investors directly with credible impact data.

Recent Developments and Capital Flows

The last twelve months were studded with notable developments. In April 2025, Bayer launched a regenerative‑agriculture program that issues removal credits while improving soil health. In January 2025, Microsoft purchased more than 3.5 million removal credits to offset emissions from AI development. Emerging markets are also innovating: Indian firm EKI Energy Services partnered with the National Dairy Development Board and Sustain Plus to monetize manure management projects for dairy farmers. Meanwhile, the Regional Voluntary Carbon Market Company (RVCMC) launched an exchange platform to scale supply and demand of high‑quality credits. These examples underscore both corporate appetite and regional dynamism.

Money is following the momentum. Over USD 10 billion was committed to new credit generation in the first half of 2025, more than three times the amount in the same period a year earlier. In capital markets, carbon credit funds, exchange‑traded products and blended finance vehicles have emerged to facilitate institutional participation. Banks are layering credits into sustainability‑linked loans and green bonds, with one USD 210 million carbon‑backed loan arranged in 2025 demonstrating how credits are becoming embedded in corporate capital allocation. Securitisation opens access to diversified portfolios, while exchange‑listed credit baskets improve liquidity and price discovery.

Drivers: What Accelerates the Voluntary Carbon Market?

Corporate net‑zero commitments remain the single biggest catalyst. More than 6,200 companies held science‑based targets in 2025, turning offsets from a discretionary purchase into a fiduciary obligation. High‑integrity standards such as the Integrity Council’s Core Carbon Principles (CCP) and the Science Based Targets initiative (SBTi) create a two‑tier market where premium credits command price premiums. Digitisation and blockchain accelerate issuance and enable real‑time MRV. Demand from new sectors such as sustainable aviation fuels and e‑fuels pushes removal credits into compliance frameworks. Finally, regional alliances such as the Asia Carbon Alliance and securitisation initiatives embed voluntary credits in mainstream finance.

Challenges: Integrity, Regulation and Volatility

While optimism abounds, the VCM is not without headwinds. A lack of pricing transparency and project‑level disclosure undermines trust. Greenwashing accusations and quality controversies have eroded market value by more than 70% between 2021 and 2024. Legal actions in the United States and reputational risk in Europe, Kenya and Singapore have spurred calls for greater accountability. Fragmented national regulations and overlapping regimes — such as the EU’s Carbon Border Adjustment Mechanism and varying Article 6 authorisations — create legal uncertainty and increase transaction costs. Price volatility persists; nature‑based credits traded between USD 7 and USD 24 per tonne entering 2026, while premium removal units can exceed USD 170–500 per tonne. These headwinds discourage smaller corporates and highlight the need for reliable platforms and robust governance.

Removal vs Avoidance: The Changing Composition of Supply

Perhaps the most profound shift heading into 2026 is the transition from cheap avoidance credits toward scarce removal credits. Analysts estimate removal credits will grow at nearly 56% CAGR , driven by biochar, bio‑energy with carbon capture and storage (BECCS), direct air capture (DAC) and high‑integrity reforestation. Nature‑based removals currently cost USD 7–24 per tonne , whereas engineered removals often exceed USD 170–500 per tonne . Waste‑methane capture projects — including landfill gas‑to‑energy systems — are slated to grow at more than 50% CAGR . Mordor Intelligence notes that avoidance and reduction credits still supply the bulk of volume, but removal projects will steadily increase their share, particularly as compliance rules for e‑fuels and sustainable aviation fuels require permanent carbon sequestration.

However, removal supply is tight, and retirements may overtake issuance before 2027. This scarcity underpins price resilience but also intensifies competition for premium credits. Portfolio diversity — blending avoidance, reduction and removal — remains essential for buyers seeking both affordability and durability.

Geographic Dynamics: Asia Surges, Europe Shapes Quality, North America Scales Finance

Asia‑Pacific is the engine of volume growth. Forecasts suggest the region could register a 36–58% CAGR , supported by massive renewable deployment, methane capture initiatives and burgeoning corporate demand. China’s reactivation of its Certified Emission Reduction scheme in 2024 unlocked roughly 250 million t CO₂ of annual issuance capacity. India’s Carbon Credit Trading Scheme transitions the country from voluntary participation to compliance, while Indonesia’s peatland restoration and regional alliances such as the Asia Carbon Alliance accelerate supply.

North America remains the largest buyer base, with a roughly 37.5% share of the voluntary market. Major U.S. corporates, especially tech giants, signed some of the largest removal deals on record. Sophisticated financial infrastructure and state‑level regulations like California’s Low‑Carbon Fuel Standard attract institutional capital via exchange‑listed funds and green bonds. Project development increasingly leans toward engineered removals and waste‑methane destruction, aligning with corporates’ permanence preferences.

Europe exerts outsized influence on price and quality. Policies such as the Carbon Border Adjustment Mechanism (CBAM), aviation emissions rules and the Green Claims Directive compel companies to prove climate claims with credible, traceable credits. EU member states champion removal‑heavy portfolios; Nordic governments blend removals with renewable‑energy certificates to achieve holistic compliance. Harmonised accounting within the bloc aids cross‑border financing, though Article 6 bilateral agreements still lag, limiting fungibility with non‑EU issuances.

Deep Dive into End Users: Beyond Corporate Buyers

Large corporates continue to dominate demand, but diversification is underway. Consumer goods and retail companies face Scope 3 emissions that exceed 98% of their footprints; as a result, they are projected to adopt voluntary credits at a 54% CAGR through 2030. Energy utilities and transport firms bundle credits with renewable‑energy certificates to decarbonise aviation and shipping. Financial institutions bundle credits into green bonds and structured loans, while hospitality groups integrate credits into carbon‑neutral guest experiences. This multisector participation reduces concentration risk and signals that the VCM is permeating mainstream business practices.

Policy and Compliance: Bridging Voluntary and Regulatory Worlds

Voluntary markets no longer operate in isolation. Article 6 of the Paris Agreement establishes a framework for authorised cross-border credit transfers, linking voluntary registries to national compliance systems. Europe’s CBAM and Refuel EU Aviation regulations embed high‑integrity credit demand into trade and transport policy. In North America, California’s AB 1305 requires public disclosure of credit attributes behind climate claims, setting a transparency precedent. Singapore’s Carbon Market Alliance aims to become a regional clearing hub for Article 6‑aligned trades. Together, these initiatives blur the line between voluntary and compliance markets, boosting confidence among institutional investors.

E‑Fuels, Aviation and Emerging Compliance Drivers

Beyond typical offset buyers, new compliance drivers are accelerating demand for removals. International Civil Aviation Organization rules require sustainable aviation fuels (SAF) to achieve up to 90% lifecycle emissions reduction. Similarly, the EU plans to raise SAF blending to 70% by 2050. Engineers working on e‑fuels (power‑to‑liquid) must integrate direct air capture credits to certify their products. These rules transform removal credits from voluntary instruments into compliance‑linked assets, creating long‑term offtake agreements and increasing project bankability.

How XGCERP Elevates Integrity and Accuracy

In a market where quality and trust determine value, XGC Corp’s XGCERP platform offers national‑grade registry capabilities with enterprise planning tools. The system connects directly to leading registries — Verra, Gold Standard, American Carbon Registry and emerging national programs — through open APIs. Every project’s issuance, transfer and retirement data flows into XGCERP in real time, eliminating double counting and enabling precise traceability. Beyond simple data aggregation, XGCERP embeds each registry’s approved mathematical methodologies into its AI engine. Baseline calculations, additionality tests, leakage adjustments and buffer pool contributions are computed automatically using the same formulas auditors expect.

This AI engine has been trained on thousands of historic projects across forestry, renewable energy, methane capture, blue carbon and regenerative agriculture. As a result, XGCERP can benchmark project performance, flag anomalies and predict credit yields with high accuracy. Automated MRV modules integrate satellite imagery, IoT sensors and on‑the‑ground data to streamline verification cycles, cutting issuance time from months to days. A built‑in digital ledger records every transaction on an immutable chain, enabling tokenisation of credits for Article 6 compliance and structured finance products. In short, XGCERP combines registry integration, methodology‑trained AI, digital MRV and blockchain provenance to offer a sovereign‑grade platform for developers, buyers and governments.

Implications for Project Developers, Buyers and Investors

For developers, 2026 offers an unprecedented opportunity. Asia‑Pacific’s scale, the shift toward removal credits and the premium attached to high‑integrity units mean that projects built on transparent data and credible methodologies will command top prices. Waste‑management and methane projects present high‑growth avenues, especially when coupled with digital MRV. For buyers, the mantra is quality first : durable, verified credits cost more but safeguard brand trust and ensure real climate impact. Buyers should diversify across project types and regions to balance price volatility with permanence.

Investors see the VCM as one of the fastest‑growing climate‑asset classes. Returns look strong thanks to supply scarcity and policy tailwinds, but diversification remains crucial given regulatory shifts and price swings. Structured finance products, carbon credit ETFs and securitised portfolios open the door to institutional capital. XGCERP’s combination of AI‑driven MRV, registry integration and blockchain provenance reduces counterparty risk and provides investors with transparent, high‑integrity assets suitable for compliance and voluntary strategies alike.

Conclusion

The voluntary carbon market stands on the cusp of its most consequential year yet. Whether one adopts the conservative forecasts of Roots Analysis or the aggressive projections of Mordor Intelligence, the direction is the same: rapid expansion, greater complexity and increasing differentiation. Project types, end‑user segments and regional growth patterns reveal a market that is fragmenting into premium and commoditised tiers. Integrity scandals and regulatory fragmentation pose challenges, but they also drive innovation, discipline and institutionalisation. With its deep registry integrations, methodology‑trained AI, automated MRV and secure digital ledger, XGCERP provides the infrastructure needed to convert climate ambition into measurable, trustworthy results. As 2026 unfolds, the combination of credible projects, robust governance and smart technology will separate winners from laggards in the race toward net zero.

Sources

- CarbonCredits.com — “Voluntary Carbon Market in 2026: Top Forecasts and What They Mean for Investors”

- Roots Analysis — Voluntary Carbon Market report page (Voluntary Carbon Credit Market Size and Industry Growth 2035)

- Mordor Intelligence — “Voluntary Carbon Credit Market Size, Share & 2025-30 Outlook”

- Bloomberg — “Trafigura Positions for ‘Huge’ Growth in Market for CO₂ Credits”